- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

Gold vs Bitcoin: Analyzing 12 Years of Data, Who Is the Real Winner?

Original Title: "Gold vs Bitcoin: 12-Year Data Tells You Who the Real Winner Is"

Original Authors: Viee, Amelia, Biteye

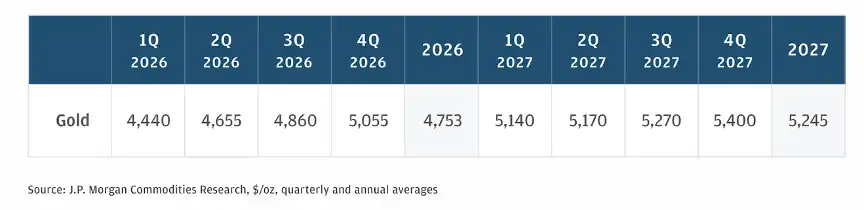

On January 29, 2026, gold plunged 3% in a single day, marking its largest recent drop. Just a few days earlier, gold had broken through $5600 per ounce to hit a new high, with silver also following suit. In the early days of 2026, prices were well above JPMorgan Chase's expectations from mid-December.

Data Source: JPMorgan Chase

In contrast, Bitcoin remained within a weak consolidation range following a pullback, further distancing itself from traditional precious metals in terms of market performance. Despite being called "digital gold," Bitcoin seems to have yet to find stability. In periods traditionally favorable to gold and silver, such as during inflation and war, Bitcoin behaves more like a risk asset, fluctuating with risk sentiment. Why is this so?

Without understanding Bitcoin's actual role in the current market structure, it is impossible to make rational asset allocation decisions.

Therefore, this article attempts to answer from multiple perspectives:

· Why has the price of precious metals surged recently?

· Why has Bitcoin underperformed significantly in the past year?

· Looking back in history, how has Bitcoin performed during gold rallies?

· For the average investor, how should one navigate this divided market environment?

1. A Game Across Cycles: The Ten-Year Showdown Between Gold, Silver, and Bitcoin

From a long-term perspective, Bitcoin remains one of the highest returning assets. However, over the past year, Bitcoin's performance has lagged notably behind gold and silver. The market trend from 2025 to early 2026 has shown a stark binary differentiation, with the precious metals market entering a phase known as a "super cycle" while Bitcoin has shown a slight decline. Below are the comparative data for three key periods:

Data Source: TradingView

Data Source: TradingView

This kind of divergent trend is not new. As early as the beginning of the COVID-19 pandemic in early 2020, gold and silver quickly surged due to safe-haven sentiment, while Bitcoin experienced a sharp drop of over 30%, followed by a rebound. During the 2017 bull market, Bitcoin surged by 1359% while gold only rose by 7%. In the 2018 bear market, Bitcoin plummeted by 63% while gold only fell by 5%. In the 2022 bear market, Bitcoin fell by 57% while gold saw a slight increase of 1%. This seems to indicate that the price correlation between Bitcoin and gold is not stable. Bitcoin appears more like an asset at the intersection of traditional finance and new finance, with both technological growth attributes and susceptibility to liquidity strength, making it harder to equate with gold, a perennial safe-haven asset.

Therefore, when we are surprised by the "digital gold not rising, real gold surging," what we really should discuss is: Is Bitcoin really considered a safe-haven asset by the market? From the current trading structure and main fund behavior, the answer may be negative. In the short term (1-2 years), gold and silver have indeed outperformed Bitcoin, but in the long term (10+ years), Bitcoin's returns are 65 times that of gold. With an extended timeframe, Bitcoin has proven with a 213-fold return that it may not be "digital gold," but it is the greatest asymmetric investment opportunity of this era.

II. Analysis of Reasons: Why Have Gold and Silver Risen More Sharply Than BTC in Recent Years?

Behind the frequent new highs in gold and silver and the lagging Bitcoin narrative is not only the divergence in price trends but also a deep deviation in asset attributes, market perception, and macro logic. We can understand the watershed between "digital gold" and "traditional gold" from the following four perspectives.

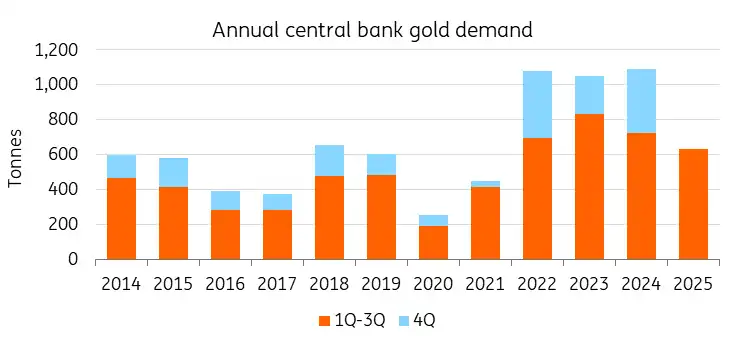

2.1. Amid a Trust Crisis, Central Banks Lead Gold Purchases

In an era of strong currency depreciation expectations, who continues to buy determines the long-term trend of the asset. From 2022 to 2024, central banks worldwide have made large-scale gold purchases for three consecutive years, with an average annual net purchase of over 1,000 tons. Whether it is emerging markets like China and Poland or resource-rich countries like Kazakhstan and Brazil, they all view gold as a core reserve asset to hedge against dollar risk. The key is that the higher the price rises, the more central banks buy—this "buy more as it gets more expensive" behavior pattern reflects the central banks' steadfast belief in gold as the ultimate reserve asset. Bitcoin struggles to gain central bank recognition, which is a structural issue: gold has a 5,000-year consensus and does not rely on any country's credit, while Bitcoin requires electricity, a network, and private keys, making central banks hesitant to allocate on a large scale.

Data Source: World Gold Council, ING Research

2.2 Gold-Silver Reversion to "Physical First"

As global geopolitical conflicts continue to escalate and financial sanctions are frequently imposed, asset security will become a question of whether they can be cashed out. After the new U.S. government took office in 2025, policies such as high tariffs and export restrictions were frequently implemented, disrupting the global market order. Gold naturally became the only ultimate asset that does not rely on another country's credit. At the same time, the value of silver in the industrial sector began to unfold: the expansion of industries such as new energy, AI data centers, and photovoltaic manufacturing increased the industrial demand for silver, driven by a real supply-demand mismatch. In this scenario, silver speculation and fundamentals resonate, leading to a more vigorous rise compared to gold.

2.3 Bitcoin's Structural Dilemma: From "Safe Haven Asset" to "Leveraged Tech Stock"

Previously, people thought of Bitcoin as a tool to combat central bank money printing. However, with the approval of ETFs and institutional entry, the fund structure has undergone a fundamental change. Wall Street institutions include Bitcoin in their portfolios, usually as a "highly elastic risk asset." We can see from the data that in the second half of 2025, Bitcoin's correlation with U.S. tech stocks reached 0.8, an unprecedented high correlation, indicating that Bitcoin is becoming more like a leveraged tech stock. When risks arise in the market, institutions are more willing to sell Bitcoin for cash, unlike gold, which is bought.

Data Source: Bloomberg

What is more representative is the liquidation during the crash on October 10, 2025, where $19 billion in leveraged positions was liquidated in one go. Bitcoin did not demonstrate its safe haven property but instead experienced a collapse due to its high leverage structure.

2.4 Why Is Bitcoin Still Falling?

In addition to the structural dilemma, there are three underlying reasons for Bitcoin's recent continued decline:

1️⃣ Crypto Ecosystem Predicament, AI Taking Over Business. The development of the crypto ecosystem has severely lagged behind. While the AI sector is attracting massive investments, the crypto world's "innovations" are still playing with memes. There are no killer applications, no real demand, only speculation.

2️⃣ Shadow of Quantum Computing. The threat of quantum computing is not baseless. Although true quantum decryption will take many years, this narrative has made some institutions hesitant. Google's Willow chip has already demonstrated quantum advantages, and although the Bitcoin community is researching post-quantum signature schemes, upgrades require community consensus, slowing down the post-quantum process but also making the network more robust.

3️⃣OGs are selling off. Many early Bitcoin holders are exiting. They feel that Bitcoin has become "tainted" — transitioning from a decentralized idealistic currency to Wall Street's speculative tool. After the ETF approval, Bitcoin's core spirit seems to be lost. MicroStrategy, BlackRock, Fidelity...Institutional holdings are growing, and Bitcoin's price is no longer determined by retail investors but by institutions' balance sheets. This is both a positive (liquidity) and a curse (losing its original purpose).

III. In-Depth Analysis: The Historical Relationship Between Bitcoin and Gold

By examining the historical relationship between Bitcoin and gold, it is found that their price correlation during major economic events is quite limited, with their performance often diverging. Therefore, the term "digital gold" is repeatedly mentioned not necessarily because Bitcoin truly resembles gold, but because the market needs a familiar reference point.

First, Bitcoin's correlation with gold was not a safe-haven resonance from the beginning. In the early days, Bitcoin was still in its infancy within the geek community, with its market value and attention minuscule. In 2013, during the banking crisis in Cyprus with some capital control measures implemented, the price of gold plummeted by about 15% from its peak; meanwhile, Bitcoin surged to over $1,000. Some interpreted this as capital flight and safe-haven funds flowing into Bitcoin. However, in hindsight, the 2013 Bitcoin frenzy was largely driven by speculation and early sentiment, and its safe-haven attributes were not widely recognized. The significant drop in gold and surge in Bitcoin that year led to a very low correlation — a monthly return correlation of only 0.08, almost zero.

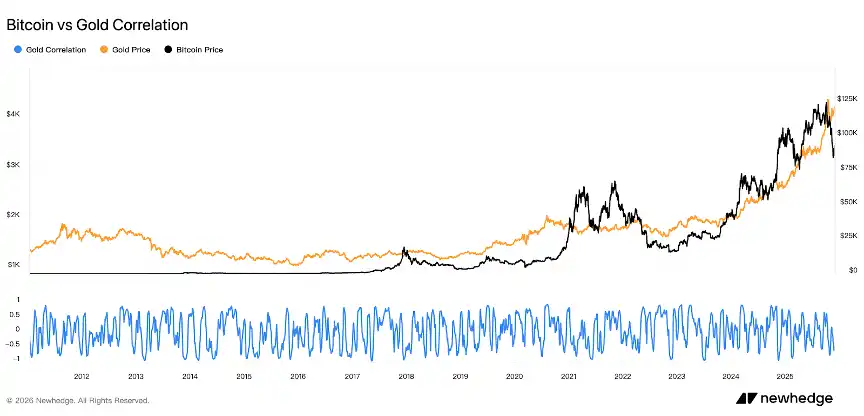

Second, true synchrony only occurred during the liquidity flood stage. After the 2020 pandemic, central banks worldwide unprecedentedly injected liquidity, causing investors to increasingly worry about fiat currency overissuance and inflation. Both gold and Bitcoin strengthened. In August 2020, the price of gold hit a then-historic high (surpassing $2,000), while Bitcoin broke $20,000 by the end of 2020, then rapidly surged above $60,000 in 2021. Many believe that during this period, Bitcoin began to demonstrate its "inflation-resistant" digital gold property, benefiting like gold from loose monetary policies worldwide. However, it should be noted that fundamentally, the loose environment provided a common ground for both to rise. Bitcoin's volatility is much higher than that of gold (annualized volatility of 72% vs. 16%).

Third, the long-term correlation between Bitcoin and gold is unstable, and the digital gold narrative is yet to be validated. Data shows that the correlation between gold and Bitcoin has been fluctuating for an extended period and, overall, is not stable. Especially after 2020, while their prices sometimes rise simultaneously, their correlation has not significantly strengthened but often shows negative correlations. This indicates that Bitcoin has not consistently played the role of "digital gold," and its trend is mainly driven by independent market logic.

Data Source: Newhedge

Upon review, it is evident that gold is a repeatedly verified safe-haven asset in history, while Bitcoin is more like an unconventional hedging tool that only stands in a specific narrative. When a crisis truly strikes, the market will still prioritize certainty over imaginative space.

IV. The Essence of Bitcoin: Not Digital Gold, But Digital Liquidity

Let's look at it from a different perspective: What role should Bitcoin really play? Is it truly meant to exist as "digital gold"?

Firstly, the underlying properties of Bitcoin determine its fundamental difference from gold. Gold is physically scarce, independent of a network, and system-free, making it a true doomsday asset. In the event of a geopolitical crisis, gold can be physically delivered at any time, serving as the ultimate safe haven. Bitcoin, on the other hand, is built on electricity, a network, and computational power, with ownership relying on private keys and transactions depending on network connectivity.

Secondly, Bitcoin's market performance is increasingly resembling that of a high-resilience tech asset. During times of ample liquidity and rising risk appetite, Bitcoin often leads the gains. However, in an environment of rising interest rates and heightened risk aversion, institutions may also reduce their Bitcoin holdings. The current market tendency is to believe that Bitcoin has not truly transformed from a "risk asset" to a "safe-haven asset" yet. It exhibits both a high-growth, high-volatility speculative aspect and a safe-haven aspect that can withstand uncertainty. This "risk-to-safe-haven" ambiguity may only be clarified through more cycles and more crises. Before that, the market still tends to view Bitcoin as a high-risk, high-return speculative asset, associating its performance with that of tech stocks.

Perhaps only when Bitcoin demonstrates a stable store of value similar to gold, can this perception truly be reversed. However, Bitcoin will not lose its long-term value; it still possesses scarcity, global transferability, and the institutional advantage of decentralization. It's just that in today's market environment, its positioning is more complex, serving as both a pricing anchor, a trading asset, and a speculative tool.

Key Takeaway: Gold is an inflation-resistant safe-haven asset, while Bitcoin is a growth asset with stronger yield characteristics. Gold is suitable for preserving value in times of economic uncertainty, with low volatility (16%) and minimal drawdowns (-18%), acting as an asset "ballast." Bitcoin is suitable for allocation when liquidity is abundant and risk appetite is rising, with an annualized return of up to 60.6%. However, it also comes with high volatility (72%) and a significant drawdown of up to -76%. This is not an either-or choice but a combination of asset allocation.

V. KOL Insights Compilation

During this round of macro repricing, gold and Bitcoin are playing different roles. Gold is more like a "shield," used to withstand external shocks such as war, inflation, sovereign risk, while Bitcoin is like a "spear," seizing the value-added opportunities of technological change.

OKX CEO Xu Mingxing @star_okx emphasized that gold is a product of old trust, while Bitcoin is the cornerstone of future-oriented new credit. Choosing gold in 2026 is like betting on a failing system. Bitget CEO @GracyBitget stated that despite inevitable market fluctuations, Bitcoin's long-term fundamentals have not changed, and he still believes in its future performance. KOL @KKaWSB cited Polymarket's forecast data, predicting that Bitcoin will outperform gold and the S&P 500 in 2026 and believes that value realization will come.

KOL @BeiDao_98 provided an interesting technical perspective: Bitcoin's RSI compared to gold has once again fallen below 30. Historically, this signal indicates that a Bitcoin bull market is imminent. Well-known trader Vida @Vida_BWE approached it from short-term fund sentiment, believing that after the surge in gold and silver, the market is eager to find the next "dollar alternative asset." Therefore, he took a small position in BTC, betting on the FOMO sentiment of fund rotation in the next few weeks.

KOL @chengzi_95330 presented a broader narrative path. He believes that traditional hard assets such as gold and silver should first absorb the credit impact of currency devaluation, and once they fulfill their roles, then it's Bitcoin's turn to enter the scene. This "first traditional, then digital" path may be the story that the current market is unfolding.

Six. Three Recommendations for Retail Investors

Faced with the difference in price appreciation between Bitcoin, gold, and silver, the most common question for ordinary retail investors is, "Which one should I invest in?" This question does not have a standard answer, but we can provide four practical suggestions:

1. Understand the positioning of each asset and clarify the allocation purpose. Gold and silver still have a strong "hedging" property during macro uncertainty, suitable for defensive positioning; Bitcoin is currently more suitable for increasing positions when risk appetite is rising, and the technology growth logic is dominant. However, be careful not to use gold to chase overnight riches. Want to hedge against inflation and seek safe haven → Buy gold; Want long-term high returns → Buy Bitcoin (but be prepared for a -70% drawdown).

2. Do not fantasize that Bitcoin will always outperform everything. Bitcoin's growth comes from the technological narrative, fund consensus, and institutional breakthrough, not from a linear return model. It will not outperform gold, the Nasdaq, or oil every year, but in the long run, its attributes as a decentralized asset still hold value. Do not completely dismiss it during short-term drawdowns, nor go all-in blindly during surges.

3. Build a Portfolio, Embrace the Reality of Different Assets Performing in Different Cycles. If you have a weak grasp of global liquidity and limited risk tolerance, you may consider a combination of Gold ETF + a small amount of BTC to address various macro scenarios; if you have a stronger risk preference, you can also combine ETH, AI tracks, RWA, and other emerging assets to construct a higher volatility portfolio.

4. Can Gold and Silver Still Be Bought Now? Be Cautious About Chasing High Prices, Prioritize Buying the Dip. In the long run, gold, as an asset favored by global central banks, and silver, with its industrial properties, still hold allocation value during turbulent periods. However, in the short term, they have seen significant gains, facing technical correction pressure, as evidenced by gold's 3% single-day plunge on January 29. If you are a long-term investor, you may consider waiting for a pullback before gradually buying in, such as gold below $5000 and silver below $100, for phased deployment; if you are a short-term speculator, you need to pay attention to the pace, not rushing in to catch the final surge when market sentiment is at its hottest. In contrast, although Bitcoin's performance has been poor, if liquidity expectations improve in the future, it may actually present a window for buying at a low. Pay more attention to the pace, avoid chasing rallies or selling off, as this is the most crucial defensive strategy for ordinary people.

In Conclusion: Understand Positioning to Survive!

When gold rises, no one will question Bitcoin's value because of it; when Bitcoin falls, it also does not mean that gold is the only answer. In this era that is reshaping the anchor of value, no single asset can meet all needs at once.

From 2024 to 2025, gold and silver take the lead. But extending the time frame to 12 years, Bitcoin shows a 213x return, proving that it may not be the "digital gold," but it is the greatest asymmetric investment opportunity of this era. Last night's gold plunge may be the end of a short-term adjustment or the beginning of a larger correction.

However, for ordinary traders, what truly matters is understanding the role positioning behind different assets and establishing their own investment logic to survive through the cycles.

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.